Lies, damned lies, and hedge fund performance statistics

Don't piss on my leg and tell me it's raining

I wrote a few weeks back that I’d been excitedly awaiting the release of professional fund manager H1 2024 fund performance letters. That, by following these regular updates, I can observe how

“over time […] they handle those occasional (inevitable?) periods of painful under-performance relative to the market and their peers“

Now those letters start trickle in and oh boy, did the Fund Performance Reporting Gods deliver. The ability to contort history into a misleading narrative, and the utter lack of respect some funds have for their clients is astounding…

Warning: Snark inbound.

It’s tough to beat the Magnificent 7

As I predicted, fund managers’ 2024 investment returns have been more moderate than the often stellar results they achieved over the past few years. Many have posted low or even slightly negative returns YTD. (Note: my own TCS EUR portfolio currently sits in negative territory at around -5% YTD, so I don’t throw too many stones about that in particular!)

Thus far, the end-of-Q2 20241 letters2 have typically contained quite a bit of commentary about “lack of market breadth at present” and “extreme concentration — the most in 20/30/40 years — coupled with extreme price rises in a handful of tech stocks in the SP500 make it hard to compete” to explain the lag of their stock picks vs their respective benchmarks. These letters, almost without fail, assure readers that such things are temporary and bode well for their particular strategy in future. Managers will “see bargains everywhere”, and “now would be a great time to top up your account with some extra cash”, and “now is definitely not the time to consider making a withdrawal".

I mean, fund management IS a business after all, so I do understand their need to placate and calm clients as the market goes through inevitable bouts of volatility and as their client portfolios wobble around in price.

What I don’t understand, is this next bullshit…

Be wary who you would make your heroes

Some of this quarter’s letters got a little weird. Some managers, after further investigation, strike me as so disingenuous and intellectually dishonest that I am stunned and amazed they’ve managed to retain customers. Even moreso when their (what I consider to be) deceptive communications are matched by (what I consider to be) correspondingly poor investment performance.

The Weird

On the weird side, for example, there’s the guys who claim their fund performance over the period dropped from a high of 9% back down to 6% “due to the news surrounding the elections in France”3, immediately before noting “we had no direct exposure4 to French-listed stocks during the quarter”.

Huh? Your portfolio was affected by a thing that you weren’t even invested in? How does that happen? Perhaps more importantly, why wouldn’t that hurt your clients again in future?

The need to constantly explain away every short-term blip and price wiggle up and down as though there is any knowable, quantifiable reason or explanation, puzzles me. Why not just admit that a few percent decline over a few weeks is less about whether snap elections are taking place in France, and more about totally-random short-term stock price movement. Although… if your fund has trailed its benchmark by almost 50% annually for the 6 years since inception5 whilst charging fees along the way, maybe any excuse is better than no excuse6.

The Wretched

In the less “weird” and more “sinister” bucket though, we observe some funds skip the “make confusing explanations” approach and instead employ the “blatant rewriting of history and denial of fault” as their go-to move when their performance stinks and their strategies cost investors money.

Games of Statistical Deception that the big industry players play

One common criticism of larger professional investment management firms is that they often employ a deceptive technique to enhance their apparent performance. They will start by launching multiple funds with varying investment strategies. Over time, some of these funds inevitably perform poorly, while others succeed. To manipulate their track record, the big firms then quietly close down or merge the underperforming funds, effectively erasing that fund’s poor performance from the firm's history.

This practice, a kind of "intentional survivorship bias," allows the firm to present a skewed picture of skill and success to potential investors. Their remaining, better-performing funds make the overall performance statistics and investment manager skill appear more favorable than they genuinely are.

Dirty, but it happens.

Games of Statistical Deception that the lazier players play

Except our next case study, the Vltava Fund, didn’t even bother to do that. Why bother closing your fund and relaunch, when you can instead pretend that entire multi-year periods of crushing losses didn’t happen? Instead, use carefully crafted graphs and statistics to cultivate an image of skill where, arguably, none exists?

Whilst reading Vltava’s latest letter I first came across a few eyebrow-raising quotes which made me want to dig a little deeper. For example, many investors acknowledge the complex nature of banks7 and financial firms, to the extent they will often avoid investing in those sectors entirely. Vltava however, claim “Banks are relatively straightforward to value”, which got me wondering, “Who are these guys? And are they any good?”

After diving into their old letters and doing some further googling, the answers aren’t pretty.8

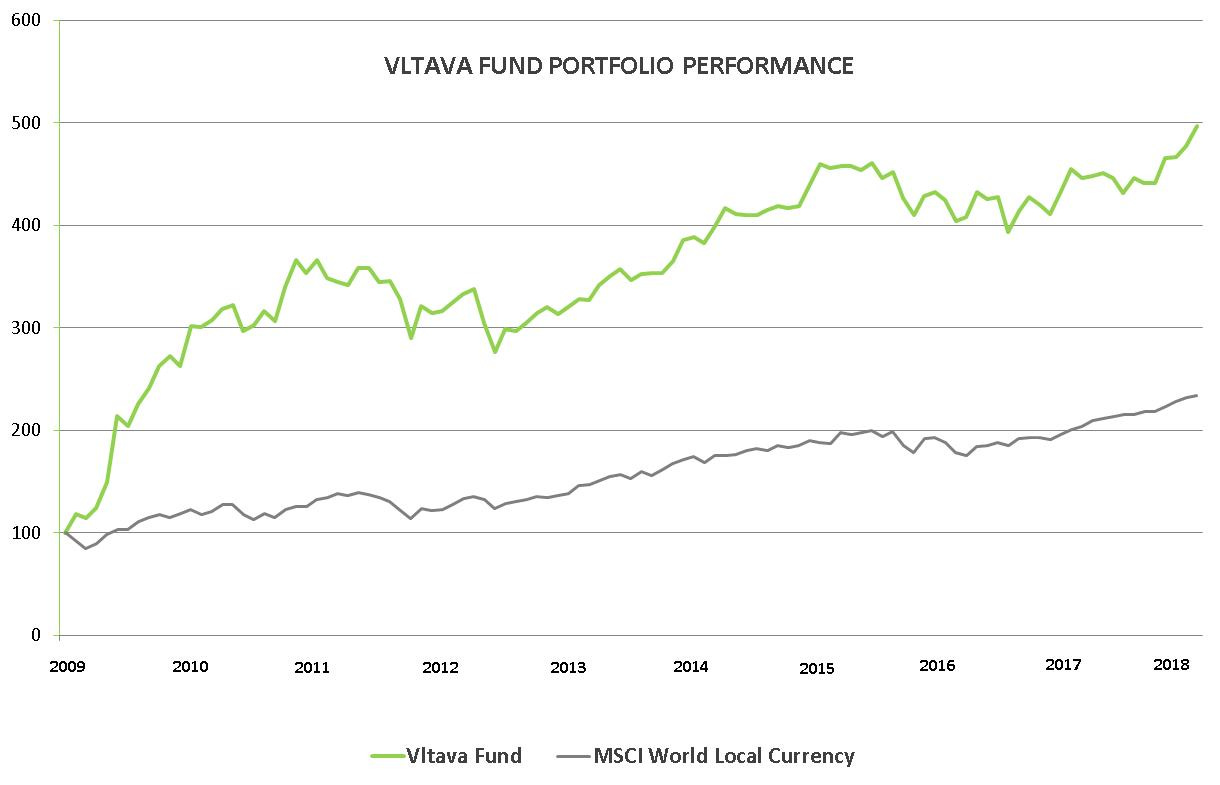

The Vltava Fund proudly declare in their marketing material that the fund more than tripled in value in 2009, with media reports that it was “the most successful fund in the world”. They further state that over the years subsequent to the GFC, the Vltava Fund total returns are vastly superior to their benchmark9. In one of their older letters, they offer the following graph to supposedly demonstrate that superior performance.

Except look closer.

It is true (and impressive) that Vltava rocketed up 200% in value over 2009, from 100 to 300. Over the next 8 years though, that 300 turned into 500, for a 66% total gain or 6.5% CAGR. The benchmark, which at first glance appears poor by comparison in the first graph, actually grows from approximately 120 to approximately 240 over the same time… for a 100% gain or 9.1% CAGR. So whilst Vltava tripled their fund value in a year in 2009 as the GFC ended, they went on to underperform their benchmark by 1/3 annually for almost the next decade.

It gets worse.

The 3 L’s: Ladies, Liquor and Leverage

You see, what I haven’t mentioned yet is that Vltava was actually founded in 2004… years before their stellar results in 2009. And how did they do over that earlier period? See the next chart. Yeah: Not great, Bob.

Even after a 200% return in 2009, their customers were STILL sitting on a roughly 50% drawdown from peak, and by 2011 were barely break-even since inception (a period of around 6 years).

So what the hell happened?

Vltava are fond of quoting Charlie Munger and Warren Buffett in their letters, which is ironic given that Vltava seem to have utterly failed to heed the warnings of the Berkshire Boys. Munger famously jokes that

“There [are] only three ways a smart person can go broke: Liquor, Ladies and Leverage. Well, the truth is – [I] only added the first two because they start with L – [there’s only one way…] it's Leverage.”

The Vltava commentary on that period, and their justifications after, read like a litany of all that is wrong with professional money management. Vltava, it turns out, had the brilliant idea that if they simply used a tonne of borrowed money (by simultaneously shorting a market index) to double the amount of stocks they bought long, they could double their returns! Hoorah, genius! And indeed, it seemed to work great — they borrowed double the money, bought twice the amount of stocks, and so achieved double the market return for 3 years… before 2008 jumped up and punched them straight in the face. Because it seems they weren’t shorting an index as described, they were shorting individual stocks, evidently, without any experience or knowledge of the risks they were taking10.

This is where things get sad and more confusing, as they largely deny any wrongdoing, and express confusion about how things went sooo bad.

See quotes like:

“How is it possible that our fund, […] for almost four years had a performance that put it among the top 10% of the global equity funds11” « Um… by using leverage to double the size of your account, you achieved double the market return. Seems pretty obvious?

“Being more conservative in this case does not necessarily mean lower future returns12” « Okay, sounds good… so why do you take more risk than necessary in the first place?

“The gross leverage and risk were kept under control,” « Said the guys that ate an 80% drawdown, “but some portion of the value was lost13” « Again, 80% drawdown after your massively leveraged bet failed, anyone?

The list goes on and on14. After the big bounce and 200% return in 2009, they decide to simply rewrite history and in future letters Vltava basically pretend that that time they borrowed a shit-tonne of money to take on extreme risk, then subsequently, disasterously, lost 80% of their client portfolios, didn’t happen. All while spouting off adjusted, selective-memory versions of events and distorted and/or misleading performance figures, and ignoring that their original customers were still sitting on a massive loss at that point!

Post-GFC newsletters carry results “stated since 2009, when we changed our strategy, so those old crashes don’t really apply…” (paraphrased, with my Snark Level set to 11 out of 10).

There’s a saying that applies here:

“Don’t piss on my leg, and tell me it’s raining.”

(meaning: don’t lie to me, telling me a situation is good for me when it is demonstrably bad)

As the earlier graph shows, even as late as 2020 a Vltava customer since 2004 inception (and arguably, even a customer that joined circa 2011 onwards) is still apparently sitting on a loss, despite the cheerful letters and hand-wavy assurances that “things are better now”. All, presumably, whilst paying fees for the privilege of achieving lower performance than a simple, low-cost index fund.

Conclusion

As you might imagine, I will be considerably more skeptical when reading fund manager letters in future. I am even more determined to own the outcomes of my own investment portfolios by presenting them in public, without massaging or manipulation of historic results. If over time it becomes evident that our Two Crows Systematic investment process sucks, I promise that you’ll hear the news from me.

And if you find yourself on the receiving end of any of the above types of wild-risk-taking-and-subsequent-loss-and-denial from your paid investment professionals, perhaps its time to consider a change of fund manager.

Footnote:

A HUGE amount of respect for the writer linked below, whose research I enjoyed and which goes into further specifics about the disappointment of finding out your investment idols actually are probably not deserving of the pedistals they stand upon.

A highly recommended read (with some extra links):

https://www.bidenko.net/the-real-performance-of-vltava-fund-sicav

https://twitter.com/JKrejci_/status/1321182752503484418

https://lettersandreviews.blogspot.com/p/2nd-quarter-2024.html

https://www.reddit.com/r/SecurityAnalysis/comments/1dyw88g/q2_2024_letters_reports/

https://gbcvalue.com/wp-content/uploads/2024/07/2024-Q2_Gehlen-Braeutigam-Value-HI-%E2%80%93-Letter-to-Partners-24-EN.pdf

Bold emphasis mine

Notably, NOT the worst underperformance observed, with one fund returning less than a 1/3 of their benchmark, the SP500, in the 6 or so years since their inception (presumably, while also collecting fees along the way)

Oops… there’s that snark I warned you about…

“Valuing banks as potential financial investments can be complex due to several unique factors within the Finance sector. Unlike other businesses, banks' financial statements are heavily influenced by regulatory requirements, risk management practices, and varying interest rate environments. Investors must consider things like the bank's net interest margin, loan-book quality, capital adequacy, and levels of non-performing assets. Additionally, banks' earnings are often impacted by macroeconomic conditions, monetary policy, political pressures, and credit cycles, making future performance harder to predict. Analysts must also understand specific banking regulations and how they affect the bank's operations and financial health. Thus, while it is possible to value banks, it requires specialized knowledge and careful consideration of multiple intricate factors.” [thank you, ChatGPT]

A HUGE amount of work and analysis into Vltava Fund was performed and reported by https://www.bidenko.net/the-real-performance-of-vltava-fund-sicav . I highly encourage you check out that post and read for a great number-crunching exposè.

More recently, other famous victims of short-selling blowups include the whole “Gamestop” saga, which you can read about https://www.nytimes.com/2022/05/18/business/melvin-capital-gamestop-short.html and https://en.wikipedia.org/wiki/GameStop_short_squeeze

https://www.vltavafund.com/dopisy-akcionarum/2008

https://www.vltavafund.com/dopisy-akcionarum/2008#:~:text=%2C%20but%20some%20portion%20of%20the%20value%20was%20lost

I invite you to trawl through their various letters here: https://www.vltavafund.com/dopisy-akcionarum